All-in-one Dashboard

Core inputs and core outputs

This comprehensive financial tool provides a complete roadmap for managing a professional claims adjusting unit from launch through five years of scaled operations.

Core inputs and core outputs

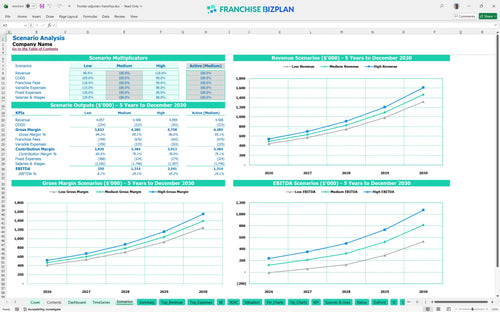

Three scenario analysis

Presentation ready

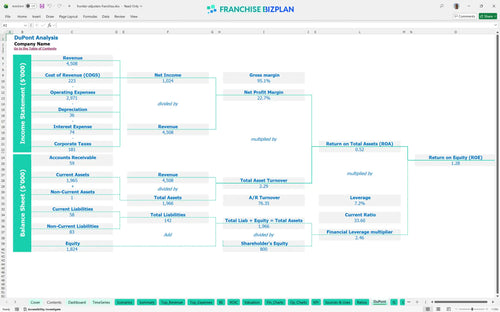

DuPont analysis

Researched revenue assumptions

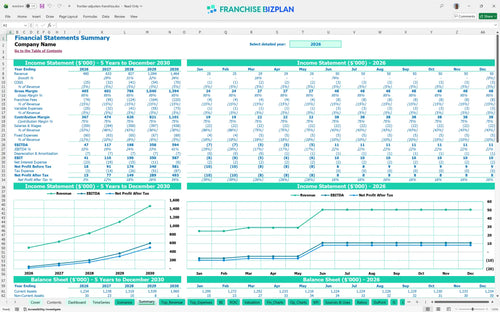

Lender-friendly financial outputs

Revenue stream detailed view

Performance metrics benchmark

We built this insurance claims franchise business plan model using our own research into the property and casualty market. Key assumptions like the $490,000 year-one revenue and the 15% royalty structure are pre-loaded but defintely editable to help you learn how to create a financial model for an insurance franchise. The model tracks everything from daily claims to catastrophe spikes to give you a realistic view of store-level margins.

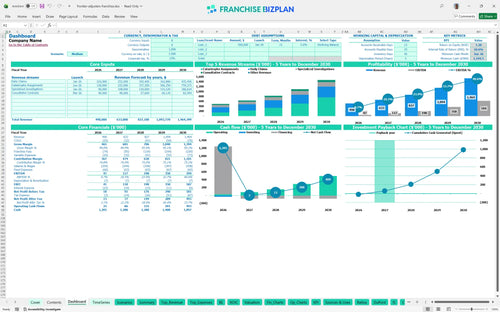

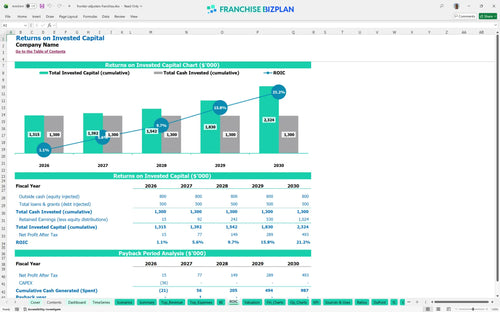

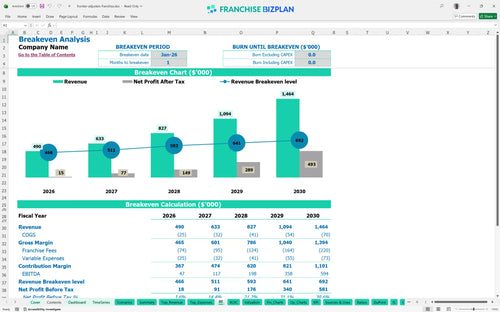

The unit reaches breakeven in January 2026, just one month after launch, and hits a full payback within two years. By year five, the franchise profitability model template projects an EBITDA of $594,000 as you scale your adjuster team. Two years to get your money back is a solid pace for this industry.

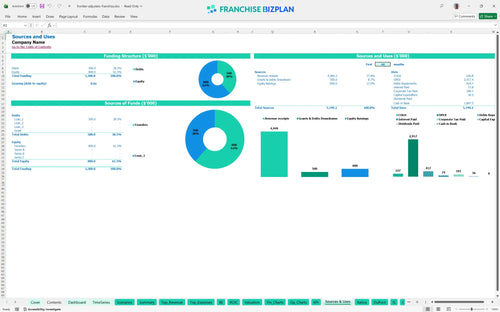

You need approximately $36,450 for the initial setup, plus a significant cash buffer for operational ramp-up. This business planning template for professional insurance services covers the $15,000 fee, a $6,000 company vehicle, and $5,000 in office improvements. You aren't just buying a desk; you're buying a field-ready operation.

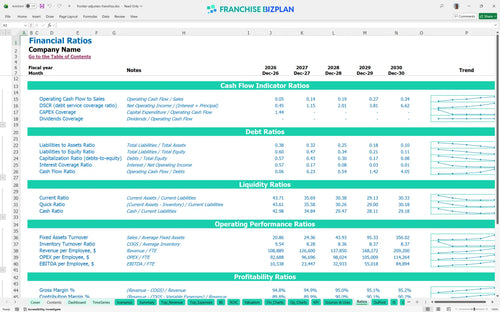

This ROI calculator for new insurance franchise investment shows an Internal Rate of Return (IRR) of 10.62% and a Return on Equity (ROE) of 1.28. With a 2-year payback, the model demonstrates how steady daily claims provide the foundation for high-margin specialized work. A 10.62% IRR beats most passive plays if you can run the desk well.

The monthly break-even point is achieved almost immediately in January 2026, driven by a strong mix of daily claims and specialized investigations. Your ability to cover the $3,000 monthly rent and 15% royalty depends heavily on maintaining a consistent referral pipeline from local agents. Volume is the engine that clears your fixed costs.

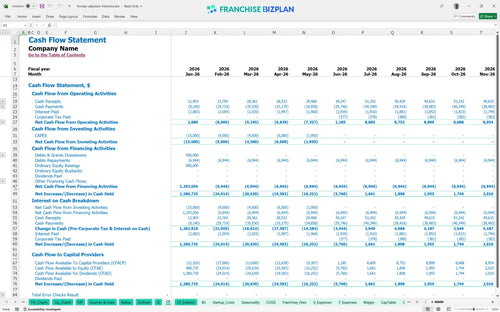

The model identifies June 2026 as the lowest cash point, with a minimum cash requirement of $1,194,000 to support high-volume catastrophe operations. Effective operational expense forecasting is critical during this window to ensure you can pay subcontractors before carrier reimbursements arrive. June 2026 is your tightest spot, so watch your billing cycles.

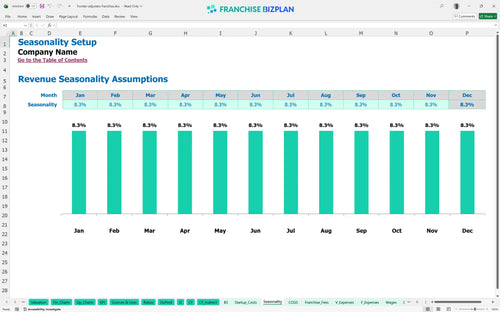

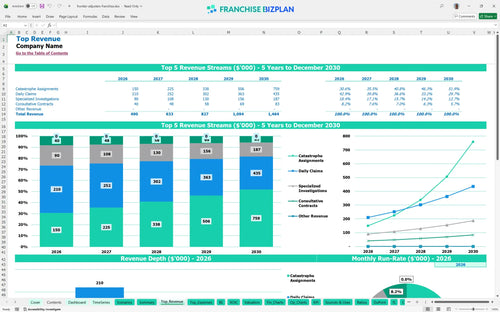

Catastrophe claims revenue modeling shows that a high-growth scenario can push year-five revenue to $1.46 million, significantly increasing your EBITDA. Low-volume years will test your 15% royalty burden, making it essential to keep fixed costs like the $3,000 rent lean. Catastrophe spikes are where the real profit is made.

Finance: update unit break-even and payback model by Friday.

This franchise financial model template is built in Excel with open formulas, allowing you to tweak every assumption to fit your specific territory. You can adjust the pre-filled data for daily claims and catastrophe work to see how different volumes impact your bottom line. Every cell is open for your specific market tweaks.

Success in the claims industry requires looking past the first storm season, so we included step-by-step financial forecasting for service franchises over a five-year horizon. These financial projections for service franchises map out your path from a $490,000 year-one start to a $1.46 million operation. Long-term visibility is the only way to manage a multi-line desk.

The model handles the heavy lifting for your franchise royalty and fee structure, specifically accounting for the 15% royalty on gross sales. By automating these calculations, you can see exactly how much cash stays in your pocket after corporate takes its cut. A 15% royalty means you have to be ruthless with your local margins.

Use this franchise startup cost spreadsheet to visualize your initial $36,450 capital outlay and identify your path to a January 2026 breakeven. It breaks down everything from the $15,000 franchise fee to office improvements and mobile tech needs. Fast breakeven is great, but cash flow is what keeps the lights on.

We integrated claims adjusting industry benchmarks to help you validate your travel expenses and subcontractor costs against typical property and casualty business metrics. This ensures your projections for field supplies and labor remain realistic as you scale your adjuster team. Don't fly blind when you can use proven industry numbers.

Simply purchase and download the financial model template, then access it instantly using Microsoft Excel or Google Sheets. No installation or technical expertise required-just open and start working.

Enter your business-specific numbers, including revenue projections, costs, and investment details. The pre-built formulas will automatically calculate financial insights, saving you time and effort.

Leverage the investor-ready format to confidently showcase your financial projections to banks, franchise representatives, or investors. Impress stakeholders with clear, data-driven insights and professional reports.

Leverage the investor-ready format to confidently present your projections to banks, franchise representatives, or investors.